Navigating the process of securing an fast personal loan can be tricky, but this guide will help you with tips on approval and finding the top interest rates.

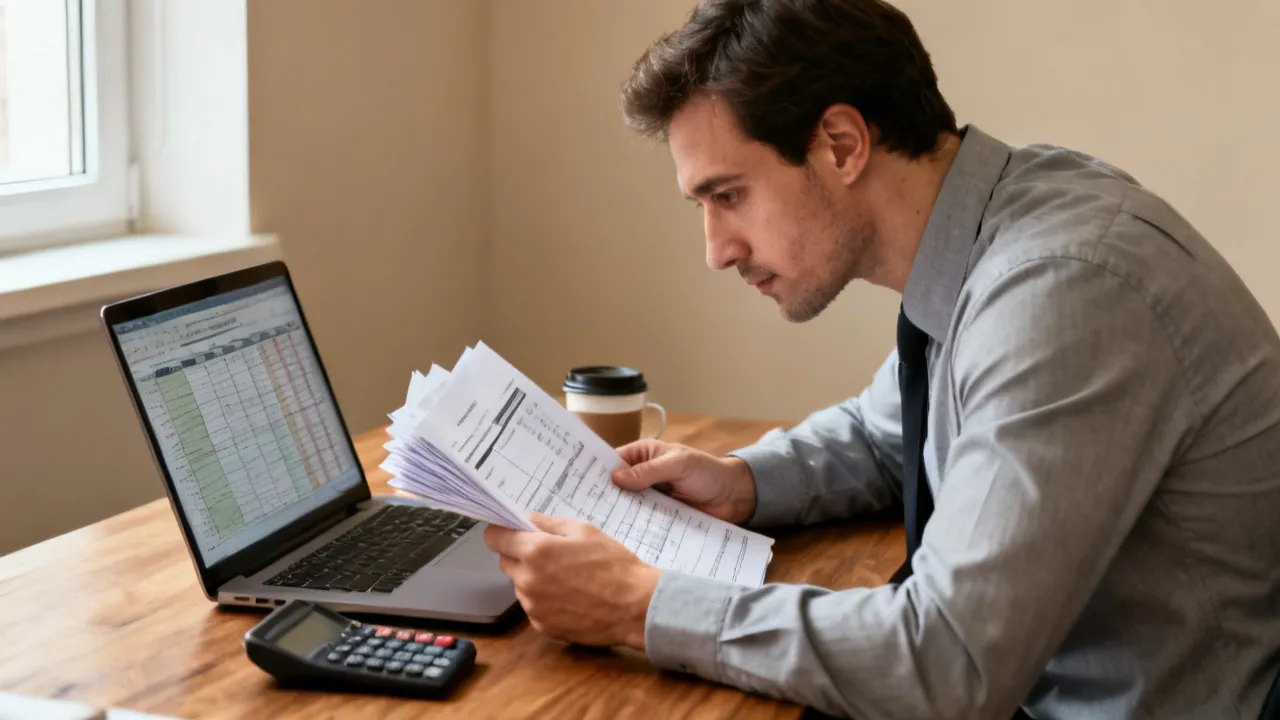

When you need a personal loan, whether for a home improvement project, medical expenses, or debt consolidation, getting approved quickly with a low-interest rate is ideal. However, securing fast approval and low rates can be challenging without understanding the process. Here’s a guide to help you maximize your chances of obtaining a personal loan with favorable terms.

Your credit score is one of the most important factors that lenders use to determine your eligibility for a personal loan, as well as the interest rate you'll be offered. A higher score generally leads to a faster approval and lower rates. To maximize your chances:

Different lenders offer different terms, so it’s important to compare rates, fees, and approval times. Consider the following:

The size of the loan and the repayment term can impact both your approval time and interest rate.

Lenders prefer knowing why you need a personal loan because it helps them assess your ability to repay. Having a clear, realistic reason for the loan, such as debt consolidation or home repairs, can help convince lenders to approve your loan faster.

Lenders want to see that you have a steady income and employment history to ensure you can repay the loan.

When applying for loans, avoid submitting multiple applications to different lenders in a short period of time. Every credit inquiry can temporarily lower your credit score, which may impact your ability to secure a low-interest loan.

Having all the required documentation on hand can speed up the approval process.

If your credit score is less than stellar, a co-signer with a higher credit score can help secure a loan with a lower interest rate. A co-signer agrees to take on the responsibility for the loan if you are unable to pay, reducing the lender’s risk and improving your chances of approval.

If you have valuable assets such as a car, property, or savings, consider applying for a secured personal loan, where you offer collateral. Secured loans typically come with lower interest rates because the lender has the assurance of recovering the asset in case you default on the loan.

Lenders often use your debt-to-income (DTI) ratio to assess your ability to handle additional debt. A DTI ratio of 36% or less is ideal for approval. This ratio is calculated by dividing your monthly debt payments by your monthly gross income.

Demonstrating your financial stability is a key factor in securing both fast approval and low rates. Keeping a clean financial record, avoiding late payments, and maintaining an emergency fund will help establish trust with lenders and prove you are a reliable borrower.

Maximizing your chances of fast personal loan approval with low interest rates requires preparation and strategy. Start by checking your credit score, shopping around for the best lender, and ensuring your finances are in order. By providing all necessary documentation, maintaining a stable income, and being realistic about the loan amount and term, you’ll improve your odds of securing an affordable loan with favorable terms. Whether it’s for an urgent need or a planned expense, being proactive and informed can make the difference in landing the loan that best suits your needs.

Unveiling Truck Fleets Near Me

Managing Efficient Truck Fleets Nearby

Understanding Truck Fleets Nearby

Understanding Truck Fleets Nearby

Navigating Truck Fleets Nearby

Navigating Truck Fleets Nearby

Navigating Truck Fleets Nearby

Understanding Truck Fleets Near Me

Navigating Truck Fleets Nearby

Navigating Bookkeeping in Modern Finance

This guide delves into the essentials of bookkeeping, a cornerstone of financial management in today's rapidly evolving economy. Bookkeeping involves the accurate and systematic recording of financial transactions, providing essential insights for personal and business financial health. Efficient bookkeeping is crucial for budget planning, tax preparation, and maintaining financial solvency.

Mastering Bookkeeping for Financial Success

This guide explores bookkeeping's integral role in maintaining financial health, offering insights into setting up bank accounts online with significant bonuses. Bookkeeping is a critical practice in financial management, ensuring accurate records of financial transactions. Understanding the benefits of various online bank accounts can optimize this process, including feasible bonus opportunities that integrate seamlessly with one's financial strategy.

Understanding Online Bank Accounts

This guide explores the intricate realm of online bank accounts, crucial for modern bookkeeping practices. Bookkeeping involves systematically recording financial transactions, providing insights into financial health and aiding strategic decision-making. Online banking has revolutionized how these transactions are conceived, executed, and tracked, enhancing accuracy and efficiency. From setting up an account to maximizing offered bonuses, this article delves deep into how various US banks facilitate this essential service.

The Essentials of Bookkeeping

This guide provides insights into the role and importance of bookkeeping, a foundational aspect of personal and business finance management. Bookkeeping involves systematically recording financial transactions to ensure accurate financial statements. In today's digital age, managing finances extends to online bank accounts, with several major banks offering incentives to new account holders.

Mastering Bookkeeping and Bank Bonuses

Bookkeeping is a critical function in finance, involving the systematic recording and tracking of financial transactions. This guide explores the role of bookkeeping in personal finance management and delves into leveraging online bank accounts to optimize financial gains. Featuring a comparison of major U.S. banks offering account opening bonuses, readers will learn how to maximize these financial incentives and integrate them into effective bookkeeping strategies for better financial management.

Analyzing Top Webbank Competitors

This article evaluates prominent online banking competitors, discussing their features, bonuses, and customer offerings. Online banking has transformed the finance sector by providing accessible and convenient banking solutions. Webbanks face stiff competition from established financial institutions that offer online account services with enticing bonuses. This analysis explores how major banks such as Bank of America, Chase, and Citibank, among others, stand their ground in this competitive landscape.