Managing credit card debt effectively is crucial for maintaining financial stability and improving your credit health.

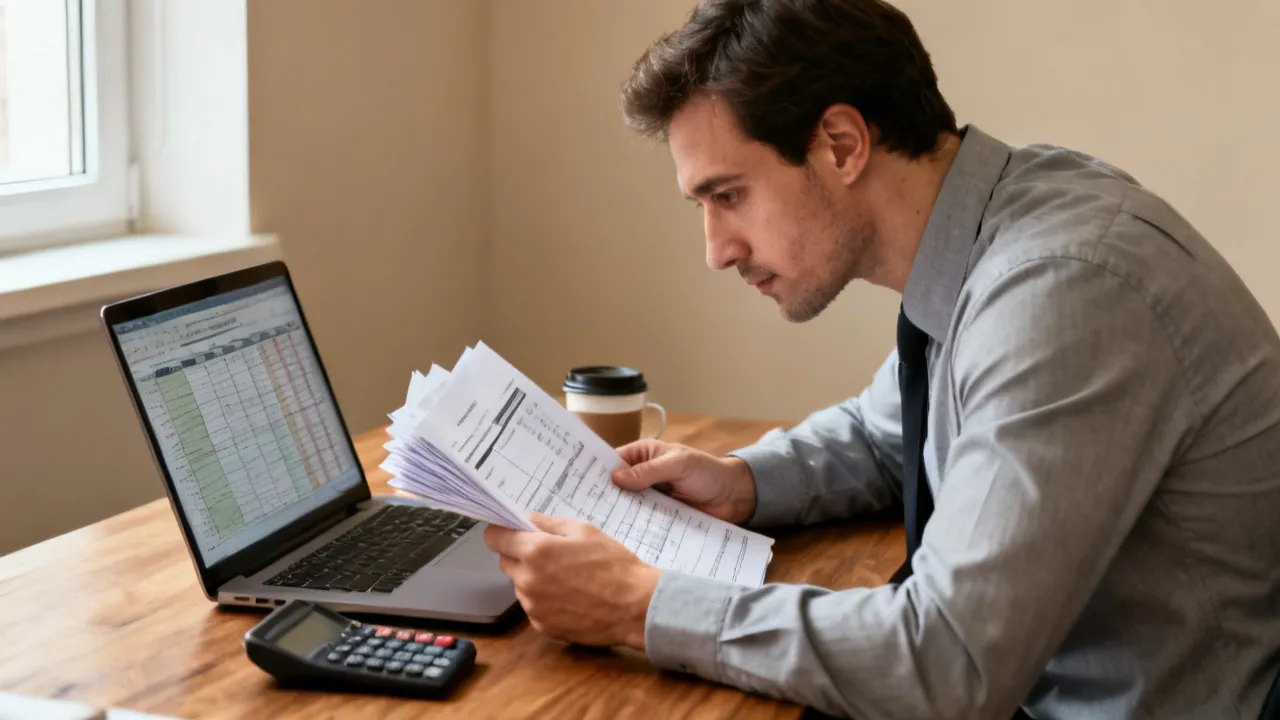

Credit card debt can quickly accumulate and become overwhelming if not managed properly. High-interest rates, late fees, and the temptation to carry balances month after month can make it difficult to pay off debt. However, with the right strategies, you can take control of your credit card debt and work towards financial freedom. Here are some smart strategies to help you effectively manage and repay your credit card debt.

The first step in managing credit card debt is understanding where your money is going. Without a budget, it's easy to overspend and let your credit card balances grow. Here’s how to start:

Paying only the minimum payment on your credit card bill can result in years of debt and thousands of dollars in interest charges. Credit card companies usually set minimum payments at a small percentage of your balance (often around 2% to 3%). While it may seem manageable, this can lead to a long repayment period and significant interest payments.

If you have balances on multiple credit cards, it’s important to tackle the ones with the highest interest rates first. This will save you the most money over time.

If you have good credit, a balance transfer credit card can be an effective strategy for saving on interest and paying down debt faster. Many credit card companies offer introductory 0% APR for balance transfers for a limited time, typically ranging from 6 to 18 months.

If you’ve been a loyal customer and have a good payment history with your credit card issuer, you may be able to negotiate a lower interest rate. A lower interest rate can significantly reduce the amount of money you pay in interest, helping you pay off your balance faster.

Missed payments can incur late fees and increase your debt due to added interest charges. One way to avoid missing payments is to automate them.

If you have multiple credit card balances and find it difficult to manage them, a debt consolidation loan can simplify your repayment process. A consolidation loan combines your credit card debts into one loan with a single monthly payment, often at a lower interest rate.

If you’re overwhelmed by your credit card debt and struggling to make progress, seeking professional help might be necessary.

One of the biggest challenges when paying off credit card debt is resisting the temptation to add to it. To successfully manage your debt, avoid adding new charges to your credit cards while you’re repaying your existing balances.

Managing credit card debt requires discipline, planning, and strategic actions. By creating a budget, paying more than the minimum, prioritizing high-interest debt, and considering tools like balance transfers or consolidation loans, you can reduce your debt more efficiently. With persistence and smart strategies, you can eliminate credit card debt and take control of your financial future.

Clara Evans

Clara is an expert editor with a deep understanding of publishing and journalism. She brings over 15 years of experience in refining content for clarity and impact. Clara has worked across various industries, from lifestyle to finance, and is committed to delivering content that is both engaging and informative.

Unveiling Truck Fleets Near Me

Managing Efficient Truck Fleets Nearby

Understanding Truck Fleets Nearby

Understanding Truck Fleets Nearby

Navigating Truck Fleets Nearby

Navigating Truck Fleets Nearby

Navigating Truck Fleets Nearby

Understanding Truck Fleets Near Me

Navigating Truck Fleets Nearby

Navigating Bookkeeping in Modern Finance

This guide delves into the essentials of bookkeeping, a cornerstone of financial management in today's rapidly evolving economy. Bookkeeping involves the accurate and systematic recording of financial transactions, providing essential insights for personal and business financial health. Efficient bookkeeping is crucial for budget planning, tax preparation, and maintaining financial solvency.

Mastering Bookkeeping for Financial Success

This guide explores bookkeeping's integral role in maintaining financial health, offering insights into setting up bank accounts online with significant bonuses. Bookkeeping is a critical practice in financial management, ensuring accurate records of financial transactions. Understanding the benefits of various online bank accounts can optimize this process, including feasible bonus opportunities that integrate seamlessly with one's financial strategy.

Understanding Online Bank Accounts

This guide explores the intricate realm of online bank accounts, crucial for modern bookkeeping practices. Bookkeeping involves systematically recording financial transactions, providing insights into financial health and aiding strategic decision-making. Online banking has revolutionized how these transactions are conceived, executed, and tracked, enhancing accuracy and efficiency. From setting up an account to maximizing offered bonuses, this article delves deep into how various US banks facilitate this essential service.

The Essentials of Bookkeeping

This guide provides insights into the role and importance of bookkeeping, a foundational aspect of personal and business finance management. Bookkeeping involves systematically recording financial transactions to ensure accurate financial statements. In today's digital age, managing finances extends to online bank accounts, with several major banks offering incentives to new account holders.

Mastering Bookkeeping and Bank Bonuses

Bookkeeping is a critical function in finance, involving the systematic recording and tracking of financial transactions. This guide explores the role of bookkeeping in personal finance management and delves into leveraging online bank accounts to optimize financial gains. Featuring a comparison of major U.S. banks offering account opening bonuses, readers will learn how to maximize these financial incentives and integrate them into effective bookkeeping strategies for better financial management.

Analyzing Top Webbank Competitors

This article evaluates prominent online banking competitors, discussing their features, bonuses, and customer offerings. Online banking has transformed the finance sector by providing accessible and convenient banking solutions. Webbanks face stiff competition from established financial institutions that offer online account services with enticing bonuses. This analysis explores how major banks such as Bank of America, Chase, and Citibank, among others, stand their ground in this competitive landscape.