Fast loans offer quick financial relief but often come with with eases and high interest rates. Here’s how to navigate them wisely.

Fast loans are convenient financial solutions designed to provide quick cash, often within hours. These loans can be lifesavers in emergencies but come with significant considerations.

One of the attractions of fast loans is the with ease aspect. However, this feature also brings potential pitfalls.

High interest rates are a hallmark of fast loans, making it crucial to understand the true cost before committing.

Below are some practical tips for managing fast loans with with ease and high interest rates:

Fast loans can be a quick fix in financial crises, but their high interest rates and with ease feature require careful consideration. By understanding the terms, evaluating your financial situation, and choosing reputable lenders, you can navigate these loans more effectively. Always explore all alternatives and plan meticulously to avoid falling into a debt trap.

Stay informed, plan wisely, and use these tips to handle fast loans effectively and responsibly.

Clara Evans

Clara is an expert editor with a deep understanding of publishing and journalism. She brings over 15 years of experience in refining content for clarity and impact. Clara has worked across various industries, from lifestyle to finance, and is committed to delivering content that is both engaging and informative.

Revolutionizing Mobility with Libercares Wheelchairs

Understanding Libercares Wheelchair Innovations

Understanding the Libercares Wheelchair

Libercares Wheelchair: Revolution in Mobility

Understanding Libercares Wheelchair Dynamics

Discovering Libercares Wheelchair

Understanding the Libercares Wheelchair

All About Libercares Wheelchair

Understanding Libercares Wheelchair Benefits

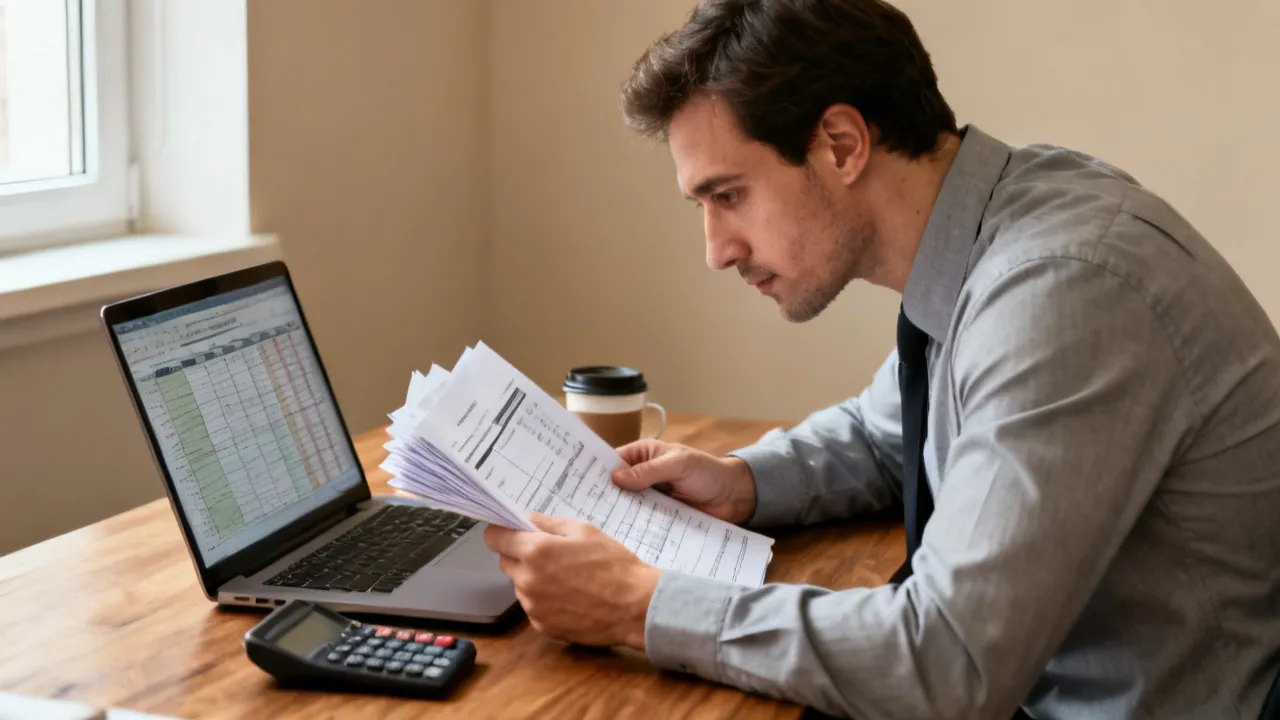

Navigating Bookkeeping in Modern Finance

This guide delves into the essentials of bookkeeping, a cornerstone of financial management in today's rapidly evolving economy. Bookkeeping involves the accurate and systematic recording of financial transactions, providing essential insights for personal and business financial health. Efficient bookkeeping is crucial for budget planning, tax preparation, and maintaining financial solvency.

Mastering Bookkeeping for Financial Success

This guide explores bookkeeping's integral role in maintaining financial health, offering insights into setting up bank accounts online with significant bonuses. Bookkeeping is a critical practice in financial management, ensuring accurate records of financial transactions. Understanding the benefits of various online bank accounts can optimize this process, including feasible bonus opportunities that integrate seamlessly with one's financial strategy.

Understanding Online Bank Accounts

This guide explores the intricate realm of online bank accounts, crucial for modern bookkeeping practices. Bookkeeping involves systematically recording financial transactions, providing insights into financial health and aiding strategic decision-making. Online banking has revolutionized how these transactions are conceived, executed, and tracked, enhancing accuracy and efficiency. From setting up an account to maximizing offered bonuses, this article delves deep into how various US banks facilitate this essential service.

The Essentials of Bookkeeping

This guide provides insights into the role and importance of bookkeeping, a foundational aspect of personal and business finance management. Bookkeeping involves systematically recording financial transactions to ensure accurate financial statements. In today's digital age, managing finances extends to online bank accounts, with several major banks offering incentives to new account holders.

Mastering Bookkeeping and Bank Bonuses

Bookkeeping is a critical function in finance, involving the systematic recording and tracking of financial transactions. This guide explores the role of bookkeeping in personal finance management and delves into leveraging online bank accounts to optimize financial gains. Featuring a comparison of major U.S. banks offering account opening bonuses, readers will learn how to maximize these financial incentives and integrate them into effective bookkeeping strategies for better financial management.

Analyzing Top Webbank Competitors

This article evaluates prominent online banking competitors, discussing their features, bonuses, and customer offerings. Online banking has transformed the finance sector by providing accessible and convenient banking solutions. Webbanks face stiff competition from established financial institutions that offer online account services with enticing bonuses. This analysis explores how major banks such as Bank of America, Chase, and Citibank, among others, stand their ground in this competitive landscape.